Daily futures contracts on RUB quoted currency pairs with automatic extension

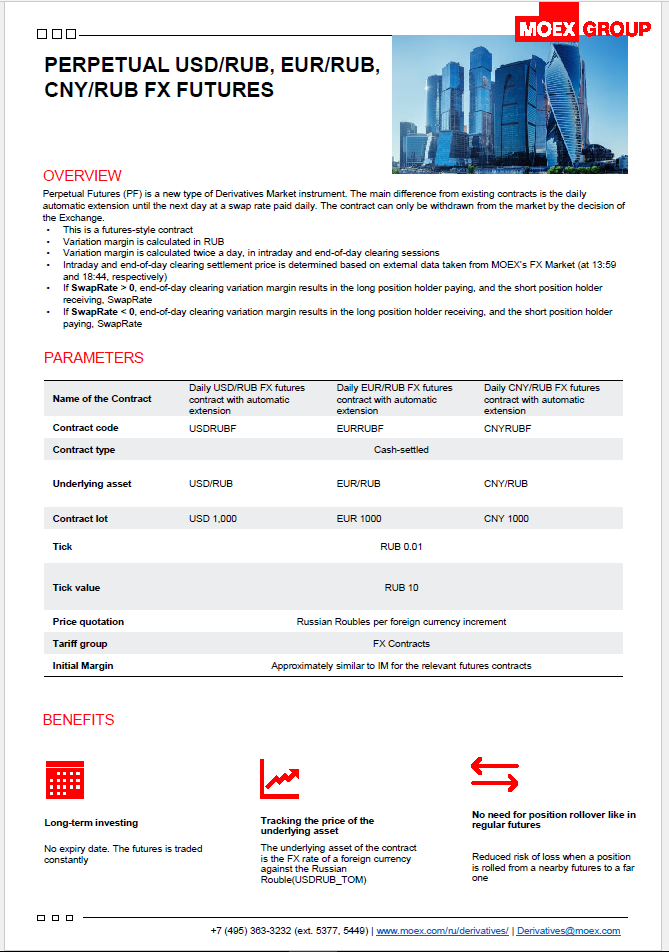

| Name of the Contract | Daily USD/RUB FX futures contract with automatic extension | Daily EUR/RUB FX futures contract with automatic extension | Daily CNY/RUB FX futures contract with automatic extension |

| Contract code | USDRUBF | EURRUBF | CNYRUBF |

| Contract type | Cash-settled | ||

| Underlying asset | USD/RUB | EUR/RUB | CNY/RUB |

| Contract lot | USD 1,000 | EUR 1000 | CNY 1000 |

| Tick | RUB 0.01 | ||

| Tick value | RUB 10/td> | ||

| Price quotation | Russian Roubles per foreign currency increment | ||

| Tariff group | FX Contracts | ||

| Initial Margin | Approximately similar to IM for the relevant futures contracts | ||

|

Suitable for long-term investing no expiry date. The futures is traded constantly |

|

Tracking the price of the underlying asset: the underlying asset of the contract is the rate of a foreign currency against the Russian rouble |

|

No need for position rollover like in conventional futures:reduced risk of loss from transferring a position from a nearby futures to a next one |

|

Managing FX open positions |

Perpetual Futures (PF) is a new type of Derivatives Market instrument. The main difference from existing contracts is the daily automatic extension until the next day at a swap rate paid daily. The contract can only be withdrawn from the market by the decision of the Exchange.

- This is a futures-style contract

- Variation margin is calculated in RUB

- Variation margin is calculated twice a day, in intraday and end-of-day clearing sessions

- Intraday and end-of-day clearing settlement price is determined based on external data taken from MOEX’s FX Market (at 13:59 and 18:44, respectively)

- If SwapRate > 0, end-of-day clearing variation margin results in the long position holder paying, and the short position holder receiving, SwapRate

- If SwapRate < 0, end-of-day clearing variation margin results in the long position holder receiving, and the short position holder paying, SwapRate

In order to ensure that the price of a futures contract always equals the FX rate of the respective currency with next day settlement as traded on MOEX’s FX Market, the swap rate for the respective currency is taken into account when calculating the variation margin.

- Example 1. Variation margin calculation at intraday and end-of day clearing

- Example 2. Calculation of variation margin when Swaprate is positive/b>

- Example 3. Calculation of variation margin when Swaprate is negative

- Example 4. Calculation of Thursday variation margin (SwapRate rolls over the weekend)

- Example 5. Calculation of Friday variation margin (SwapRate rolls over the weekend)

Derivatives Market Department

Tel.: +7 (495) 363-3232

email: derivatives@moex.com